Life insurance when buying a home

Buying a home is a big financial commitment. Find out how life insurance fits into the home buying process, what cover people often choose, and what to consider as you get ready to move.

Published: 9 July 2026

Manage your insurance policy online.

Set up your account to manage your policy.

Choose the type of claim you need to make.

Buying a home is a big financial commitment. Find out how life insurance fits into the home buying process, what cover people often choose, and what to consider as you get ready to move.

Published: 9 July 2026

There’s no law that says you must have life insurance to take out a mortgage. Some lenders may encourage you to get it, and a small number may require it as part of their lending criteria, but most of the time it’s your choice.

Many buyers still choose to take out life insurance when buying a home because:

If you’re new to life insurance, learn more about life insurance in our guide - What is life insurance?

Life insurance pays out a lump sum if you die during the policy term. Your beneficiaries can choose how to use the money, which could include:

Life insurance doesn’t automatically go to the lender. Your beneficiaries decide how the payout is used.

You can learn more about beneficiaries in our guide - What is a life insurance beneficiary?.

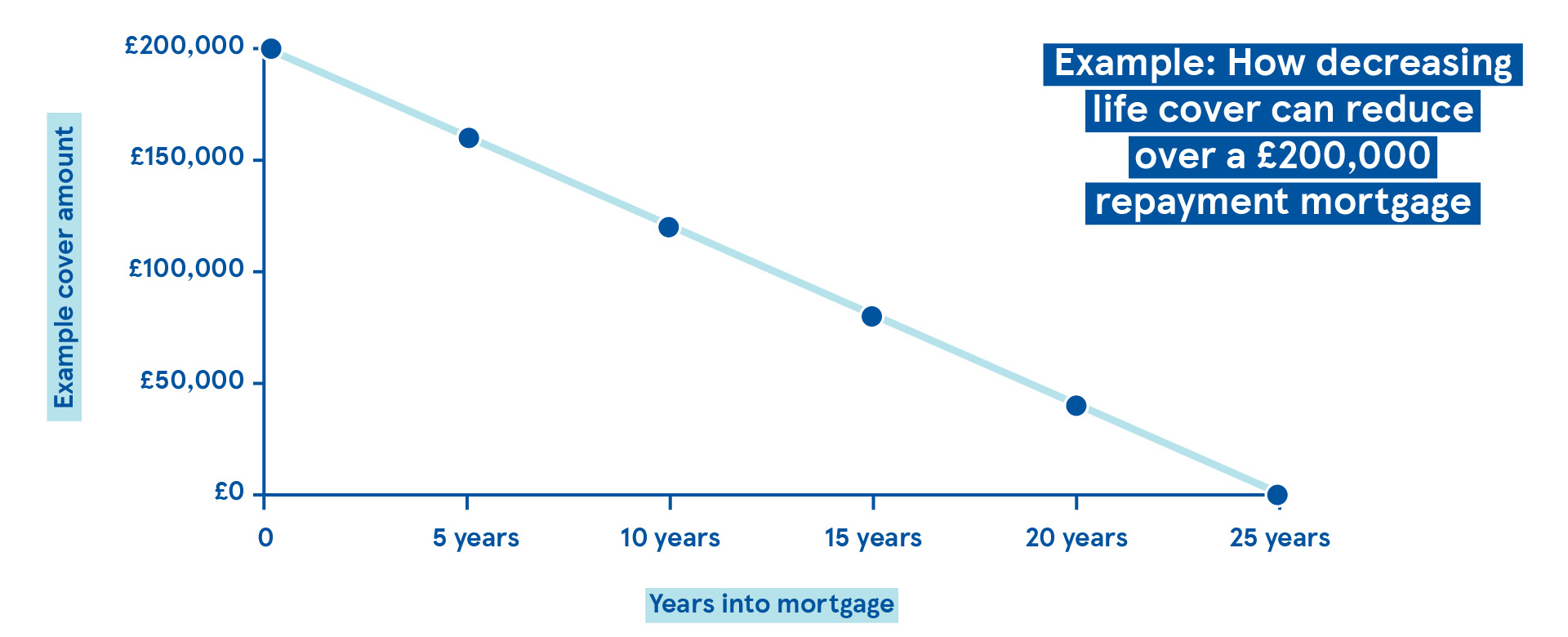

Homeowners usually choose one of two types of term life insurance: decreasing cover or level cover.

Often used for repayment mortgages.

Here's a simple example of how decreasing cover might reduce over a 25-year £200,000 repayment mortgage.

Often used for interest only mortgages or wider family protection.

To compare both types in more detail, see our guide - Types of life insurance explained.

|

Feature |

Decreasing cover |

Level cover |

|---|---|---|

|

Cover amount |

Reduces over time |

Stays the same |

|

Monthly payments |

Stay the same |

Stay the same |

|

Common use |

Repayment mortgages |

Interest only mortgages, family protection |

|

Typical cost |

Usually, lower |

Usually, higher |

|

Payout |

Matches reducing mortgage |

Fixed lump sum |

If you’re buying a home with a partner, you can choose either a joint policy or two single policies.

There’s no right or wrong choice. It depends on your shared financial responsibilities and what feels suitable.

Many people think about life insurance for the first time when moving from renting to owning. That’s because buying a home:

If you’re new to cover, see our guide - Life insurance for your family.

"Is life insurance compulsory for a mortgage?"

No, but lenders may recommend it.

"Will my mortgage lender get the payout?"

No. Life insurance, when in a trust, pays beneficiaries, not lenders.

"Does life insurance automatically clear the mortgage?"

No, but many people choose a cover amount that could help repay it.

"Do I have to buy life insurance from my mortgage broker?"

No. You’re free to choose a provider that suits you.

If you already have life insurance, a house move is a good moment to check:

Here’s a simple checklist you can use when buying a new home:

These independent sources offer practical help throughout the moving process.

There’s no set rule, but many people choose to arrange life insurance:

Arranging it earlier means you have cover in place from the beginning of your new financial responsibility.

At Tesco Insurance, we want to help you with the things that matter most. That’s why Tesco Life Insurance comes with a Big Win and lots of Little Helps.

As well as your Tesco benefits, you’ll also get Aviva DigiCare+ - a health and wellbeing service from Aviva that includes unlimited Digital GP consultations and the Bupa Anytime HealthLine.

Tesco Life Insurance is provided and administered by Aviva, who have a 5-star Defaqto rating for life insurance and pay out on 98.7% of claims*.

Get help and support online. Or find out how to contact Aviva, our life insurance provider.

Tesco Life Insurance is arranged, administered and underwritten by Aviva Life & Pensions UK Limited.

Tesco Personal Finance Ltd acts as an introducer to Aviva Life & Pensions UK Limited which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Member of the Association of British Insurers. Firm Reference Number 185896.

Aviva Life & Pensions UK Limited. Registered in England & Wales No. 3253947. Registered Office: Aviva, Wellington Row, York, YO90 1WR. Tesco Personal Finance Ltd and Aviva Life & Pensions UK Limited. are not part of the same corporate group.

Tesco Insurance is a trading name of Tesco Personal Finance Ltd, Registered Office: 2 South Gyle Crescent, Edinburgh, EH12 9FQ (registered in Scotland, no SC173199) which is authorised and regulated by the Financial Conduct Authority (register no. 186022).

With the Aviva DigiCare+ app, you can start using a range of health and wellbeing services when you take out your policy.

Members of your family can use it too, as long as they're eligible.

The Aviva DigiCare+ app is provided by Square Health. The services are provided by Square Health and other selected partners.

You'll find full details about the services in the app, along with the terms and conditions, residency restrictions and privacy policy.

Aviva DigiCare+ is a non-contractual benefit that could be changed or withdrawn by Aviva at any time. So, it won't appear in any contract you've signed, or in any terms and conditions.

Please check the policy documents to make sure the cover you’ve chosen meets your needs.

The policy booklet and product information documents tell you about the benefits, limitations and exclusions that’ll apply to your cover.

Tesco Life Insurance is provided, administered and underwritten by Aviva Life & Pensions UK Limited.

Aviva have a 5-star rating for life insurance from Defaqto. And they pay out on 98.7% of life insurance claims*.

*Aviva UK individual claims report 2026, based on claims paid in 2025.

Find the right cover to give financial support to your family after you’ve gone. Tesco Life Insurance comes with Clubcard Prices, Tesco perks and Aviva DigiCare+.